2013 UPDATE:

As of 2012/13 Forestry Tasmania have stopped reporting their average mill door log values (MDLV) by product grade, so it is no longer possible to track and report on their product sales and pricing performance. So much for greater accountability and transparency.

________________________________________________________

It is very clear from recent pricing and production from Forestry Tasmania that the special timbers industry is completely divorced from any commercial reality. The administered sales and pricing policies are sucking what little life there is left out of the industry, and consequently the blackwood industry has a very bleak future unless there is serious change.

This is the second part in my analysis of the special timbers market in Tasmania. In the first part I discussed how in 2010 Forestry Tasmania decided that henceforth their special timbers business activities would be non-profit non-commercial, and therefore deserving of a massive 50%+ taxpayer subsidy to the value of $5.1 million dollars over the past 3 years. In part one I discussed how this change of forest policy disadvantaged private forest growers, the Tasmanian community and would ultimately lead the special timbers industry down the same road as Ford Australia.

In this second part I look at the special timbers pricing and sales policies of Forestry Tasmania and how they contribute to this perfect commercial storm, effectively destroying the industry and any potential that the blackwood industry has of a prosperous, profitable future based on a farm-grown resource.

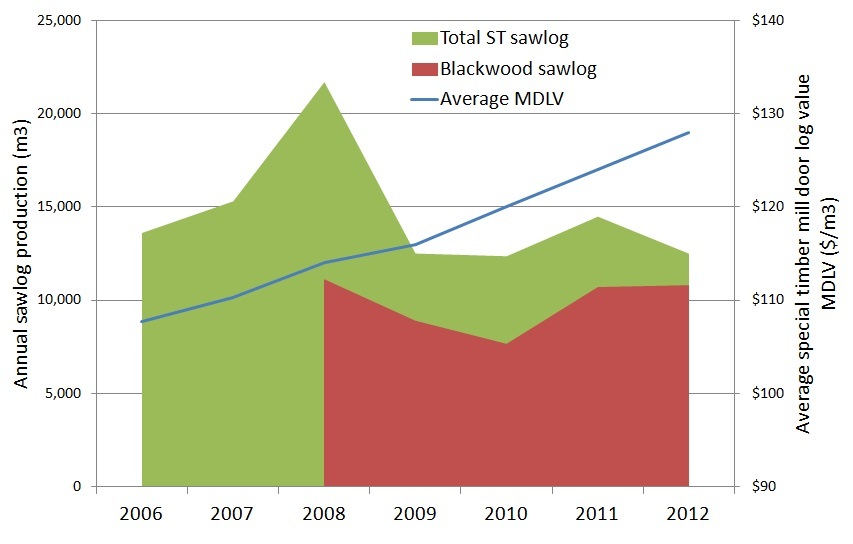

Forestry Tasmania (FT) is the major special timbers grower in Tasmania so analysing their production and revenue figures provides useful insights into the opaque world of the “administered” special timbers market. With blackwood comprising 70% of special timbers production by volume over the last 5 years this analysis is largely relevant to the blackwood market and its future. Over the last 5 years Forestry Tasmania has provided separate blackwood production figures but not separate blackwood revenue figures. The chart below shows total special timbers (ST) and blackwood production, and the average unit special timbers mill door log value (MDLV). All data is from FT annual reports.

The chart shows that the introduction by Forestry Tasmania in 2010 of the non-profit non-commercial policy plus major taxpayer subsidy appears to have had no impact on the price or production of special timbers. Certainly none of the subsidy appears to have been passed on to the rest of the industry, unless the industry was already enjoying heavily discounted prices, and FT was just seeking formal reimbursement from the Tasmanian taxpayer.

We also know that FT sells their sawlog through “administered pricing” that “are not determined by regular market forces of supply and demand”. These administered prices are even immune to global financial disasters. The global financial crisis that struck half way through the 2007-08 financial year had a significant impact on demand, with special timbers production almost halving, but had no impact on the administered price. Extraordinary!

Forestry Tasmania provides no information on what basis they determine administered special timbers sawlog prices. With a non-profit business objective and a generous taxpayer subsidy the administered special timbers sawlog pricing policy is anything but clear.

What is clear from the above chart is that special timbers sawlog prices are basically indexed to inflation. Over the above 7 year period sawlog prices increased by an average 3.4% per annum – the long-term inflation rate. In other words special timbers prices are not determined by regular market forces of supply and demand, and do not increase in real terms over time. If that is not a disincentive to private growers and investment I don’t know what is!

All of this has little relevance except for the fact that:

- blackwood is the dominant special timber species;

- blackwood is common on many Tasmanian farms;

- farmers already sell small quantities of blackwood into the special timbers market in competition with dedicated non-profit Forestry Tasmania;

- blackwood is the only Tasmanian special timber species that has the potential to be grown profitably by farmers to grow and develop the blackwood industry as farmers are doing in New Zealand; and

- All the other special timber species are too slow growing, and too rare on Tasmanian farms to be of commercial importance.

So what does the above chart mean for blackwood sawlog prices and the blackwood market in the Tasmania?

- Blackwood sawlog prices in Tasmania are dominated by Forestry Tasmania and are clearly heavily discounted to the point where even a global financial disaster has no impact.

- With prices having absolutely no connection to any market reality it reinforces the understanding developed in Part 1 that the blackwood market is effectively closed to private growers and investment.

Another useful perspective special timbers pricing is gained from looking at tender prices achieved by Forestry Tasmania subsidiary Island Specialty Timbers (IST). IST provides the only market-based special timbers price information available anywhere. IST only tender a tiny volume of special timbers every year (less than 100 cubic metres) so their tender results may not represent actual market conditions. But if the tenders are competitive and the results show the best offers received then they are much more indicative of real current market value than the FT administered price. IST doesn’t produce any regular market report or annual report so tracking their performance is impossible.

What is clear is that there is a significant disparity between the IST tender results and the average administered price received by Forestry Tasmania ($128 per cubic metre in 2012). Obviously Forestry Tasmania does not use its own tender results to inform their administered pricing rules, and why the special timbers industry is receiving a massive taxpayer subsidy while these price discrepancies exist raises serious questions.

Presumably blackwood administered sawlog prices are less than the average price of $128/m3, due to it’s greater availability and quicker growth rates compared to the other species. However given the dominance and the importance of the blackwood market to the future of the special timber industry and to private growers IST provides scant information on this species. Current tender results for plain-grain blackwood sawlogs range from $250 – $450 per cubic metre, significantly higher than $128. This shows that the market is prepared to pay significantly more than the administered price for special timbers. But to help gain greater accuracy, detail and transparency into the blackwood market IST should be tendering at least 500 cubic metres of blackwood sawlog per year and publishing more detailed and regular market reports.

If Forestry Tasmania’s administered pricing more closely reflected IST tender results we could potentially have a tripling of FT special timbers revenue. The industry would then be transparently profitable, no longer in need of a significant public subsidy and would instead contribute revenue to the State Treasury and the community.

These changes would also provide significant stimulus into the blackwood market, Tasmanian farmers would be selling more blackwood at higher prices and wondering how to grow more. And that is where the blackwood growers cooperative proposal becomes important.

To help put these special timbers sawlog prices into some perspective (which is not easy as sawlog prices in Australia are extremely opaque, while New Zealand sawlog prices are very transparent), current NZ Pinus radiata pruned sawlogs are $AU103 per cubic metre at wharf (allowing for differences in the exchange rate), while NZ unpruned douglas fir sawlog at wharf is $AU96. Pruned, farm-grown NZ Cupressus macrocarpa sawlogs are $AU240 per cubic metre at mill door, with macrocarpa grown on ~35 year rotations. Based on these comparisons Forestry Tasmania’s administered prices for our premium timbers are very shabby indeed and do not justify any public subsidy.

For the past 2 years I have been trying to understand why blackwood, a product that has been a quality Tasmanian icon for over 100 years, seems to have so little market activity, profile, price or transparency. Blackwood isn’t just an icon, it’s an enigma.

The commercial management of the special timbers industry by Forestry Tasmania and the State government is an unqualified disaster. The accounting, sales and pricing policies of Forestry Tasmania are directly inhibiting blackwood investment, destroying the special timbers industry and costing the Tasmanian community money at a time when the State can least afford it.

So what do you think?

Is Tasmania getting a fair deal for its public special timbers resource?

Do you think the industry has a great future as a profitable commercial Tasmanian icon?

Should FT change its sales and pricing policies to give Tasmanians and Tasmanian farmers a better deal for their special timbers?

Is a consumer boycott of the special timbers industry needed to motivate the industry to change?

Collective marketing of Tasmanian blackwood?

This is an interesting article from the latest New Zealand Tree Grower journal from the New Zealand Farm Forestry Association, and potentially represents a significant milestone in the fledgling NZ blackwood industry.

Alan Laurie runs Laurie Forestry Ltd a progressive and commercially focused forest management, harvesting and marketing business. I always enjoy reading Alan’s regular forestry market reports that always me to know much more about what is happening with the NZ forest industry than I know about the industry here in Australia.

For Alan to make these comments about the potential of New Zealand blackwood is a significant vote of confidence in the industry. While there is a blackwood interest group (AMIGO) established under the NZFFA, they have yet to evolve into a marketing cooperative despite the fact that steady volumes of quality NZ blackwood timber are now coming onto the NZ market. Certainly what needs to happen soon is greater market transparency and feedback, so that prices and return on investment allow more potential blackwood growers to take an interest and help build the industry.

Blackwood appears to be an ideal tree species with which to begin collective marketing. The timber has the obvious market advantage of being in limited supply but appears to be in constant demand. Demand may increase slightly if a constant supply is guaranteed and imports of blackwood timber are very expensive.

To this comment from Alan Laurie I would also add that blackwood also has the advantage of a well established market presence and profile as a premium quality timber, so marketing and sales should be straight forward, compared to many lesser-known species.

So can the NZFFA/AMIGO evolve into a marketing cooperative and help take the NZ blackwood industry to the next level?

I would think given Alan Laurie’s knowledge, experience and place in the industry he could play a pivotal role in making the collective marketing happen.

Leave a comment

Posted in Commentary, Markets, New Zealand