2013 UPDATE:

As of 2012/13 Forestry Tasmania have stopped reporting their average mill door log values (MDLV) by product grade, so it is no longer possible to track and report on their product sales and pricing performance. So much for greater accountability and transparency.

________________________________________________________

It is very clear from recent pricing and production from Forestry Tasmania that the special timbers industry is completely divorced from any commercial reality. The administered sales and pricing policies are sucking what little life there is left out of the industry, and consequently the blackwood industry has a very bleak future unless there is serious change.

This is the second part in my analysis of the special timbers market in Tasmania. In the first part I discussed how in 2010 Forestry Tasmania decided that henceforth their special timbers business activities would be non-profit non-commercial, and therefore deserving of a massive 50%+ taxpayer subsidy to the value of $5.1 million dollars over the past 3 years. In part one I discussed how this change of forest policy disadvantaged private forest growers, the Tasmanian community and would ultimately lead the special timbers industry down the same road as Ford Australia.

In this second part I look at the special timbers pricing and sales policies of Forestry Tasmania and how they contribute to this perfect commercial storm, effectively destroying the industry and any potential that the blackwood industry has of a prosperous, profitable future based on a farm-grown resource.

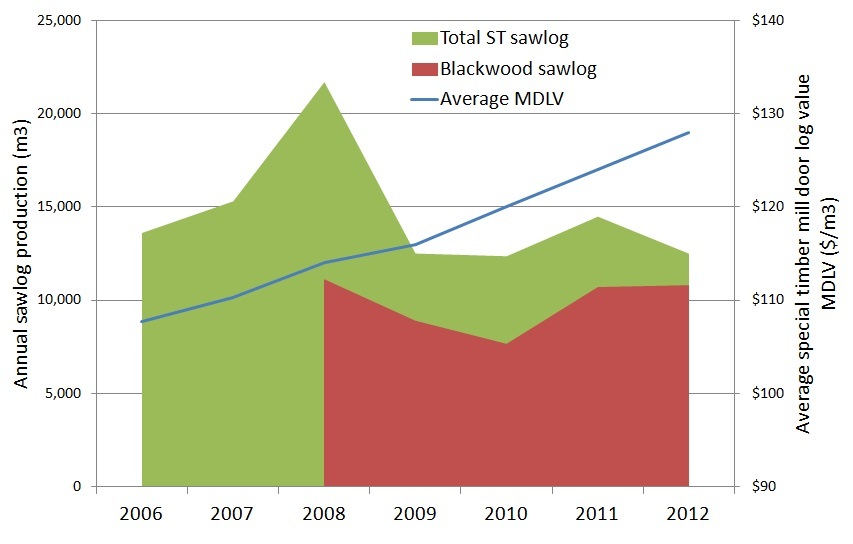

Forestry Tasmania (FT) is the major special timbers grower in Tasmania so analysing their production and revenue figures provides useful insights into the opaque world of the “administered” special timbers market. With blackwood comprising 70% of special timbers production by volume over the last 5 years this analysis is largely relevant to the blackwood market and its future. Over the last 5 years Forestry Tasmania has provided separate blackwood production figures but not separate blackwood revenue figures. The chart below shows total special timbers (ST) and blackwood production, and the average unit special timbers mill door log value (MDLV). All data is from FT annual reports.

The chart shows that the introduction by Forestry Tasmania in 2010 of the non-profit non-commercial policy plus major taxpayer subsidy appears to have had no impact on the price or production of special timbers. Certainly none of the subsidy appears to have been passed on to the rest of the industry, unless the industry was already enjoying heavily discounted prices, and FT was just seeking formal reimbursement from the Tasmanian taxpayer.

We also know that FT sells their sawlog through “administered pricing” that “are not determined by regular market forces of supply and demand”. These administered prices are even immune to global financial disasters. The global financial crisis that struck half way through the 2007-08 financial year had a significant impact on demand, with special timbers production almost halving, but had no impact on the administered price. Extraordinary!

Forestry Tasmania provides no information on what basis they determine administered special timbers sawlog prices. With a non-profit business objective and a generous taxpayer subsidy the administered special timbers sawlog pricing policy is anything but clear.

What is clear from the above chart is that special timbers sawlog prices are basically indexed to inflation. Over the above 7 year period sawlog prices increased by an average 3.4% per annum – the long-term inflation rate. In other words special timbers prices are not determined by regular market forces of supply and demand, and do not increase in real terms over time. If that is not a disincentive to private growers and investment I don’t know what is!

All of this has little relevance except for the fact that:

- blackwood is the dominant special timber species;

- blackwood is common on many Tasmanian farms;

- farmers already sell small quantities of blackwood into the special timbers market in competition with dedicated non-profit Forestry Tasmania;

- blackwood is the only Tasmanian special timber species that has the potential to be grown profitably by farmers to grow and develop the blackwood industry as farmers are doing in New Zealand; and

- All the other special timber species are too slow growing, and too rare on Tasmanian farms to be of commercial importance.

So what does the above chart mean for blackwood sawlog prices and the blackwood market in the Tasmania?

- Blackwood sawlog prices in Tasmania are dominated by Forestry Tasmania and are clearly heavily discounted to the point where even a global financial disaster has no impact.

- With prices having absolutely no connection to any market reality it reinforces the understanding developed in Part 1 that the blackwood market is effectively closed to private growers and investment.

Another useful perspective special timbers pricing is gained from looking at tender prices achieved by Forestry Tasmania subsidiary Island Specialty Timbers (IST). IST provides the only market-based special timbers price information available anywhere. IST only tender a tiny volume of special timbers every year (less than 100 cubic metres) so their tender results may not represent actual market conditions. But if the tenders are competitive and the results show the best offers received then they are much more indicative of real current market value than the FT administered price. IST doesn’t produce any regular market report or annual report so tracking their performance is impossible.

What is clear is that there is a significant disparity between the IST tender results and the average administered price received by Forestry Tasmania ($128 per cubic metre in 2012). Obviously Forestry Tasmania does not use its own tender results to inform their administered pricing rules, and why the special timbers industry is receiving a massive taxpayer subsidy while these price discrepancies exist raises serious questions.

Presumably blackwood administered sawlog prices are less than the average price of $128/m3, due to it’s greater availability and quicker growth rates compared to the other species. However given the dominance and the importance of the blackwood market to the future of the special timber industry and to private growers IST provides scant information on this species. Current tender results for plain-grain blackwood sawlogs range from $250 – $450 per cubic metre, significantly higher than $128. This shows that the market is prepared to pay significantly more than the administered price for special timbers. But to help gain greater accuracy, detail and transparency into the blackwood market IST should be tendering at least 500 cubic metres of blackwood sawlog per year and publishing more detailed and regular market reports.

If Forestry Tasmania’s administered pricing more closely reflected IST tender results we could potentially have a tripling of FT special timbers revenue. The industry would then be transparently profitable, no longer in need of a significant public subsidy and would instead contribute revenue to the State Treasury and the community.

These changes would also provide significant stimulus into the blackwood market, Tasmanian farmers would be selling more blackwood at higher prices and wondering how to grow more. And that is where the blackwood growers cooperative proposal becomes important.

To help put these special timbers sawlog prices into some perspective (which is not easy as sawlog prices in Australia are extremely opaque, while New Zealand sawlog prices are very transparent), current NZ Pinus radiata pruned sawlogs are $AU103 per cubic metre at wharf (allowing for differences in the exchange rate), while NZ unpruned douglas fir sawlog at wharf is $AU96. Pruned, farm-grown NZ Cupressus macrocarpa sawlogs are $AU240 per cubic metre at mill door, with macrocarpa grown on ~35 year rotations. Based on these comparisons Forestry Tasmania’s administered prices for our premium timbers are very shabby indeed and do not justify any public subsidy.

For the past 2 years I have been trying to understand why blackwood, a product that has been a quality Tasmanian icon for over 100 years, seems to have so little market activity, profile, price or transparency. Blackwood isn’t just an icon, it’s an enigma.

The commercial management of the special timbers industry by Forestry Tasmania and the State government is an unqualified disaster. The accounting, sales and pricing policies of Forestry Tasmania are directly inhibiting blackwood investment, destroying the special timbers industry and costing the Tasmanian community money at a time when the State can least afford it.

So what do you think?

Is Tasmania getting a fair deal for its public special timbers resource?

Do you think the industry has a great future as a profitable commercial Tasmanian icon?

Should FT change its sales and pricing policies to give Tasmanians and Tasmanian farmers a better deal for their special timbers?

Is a consumer boycott of the special timbers industry needed to motivate the industry to change?

A meeting with Forestry Tasmania

I had a meeting last week with representatives of Forestry Tasmania (FT) to discuss special timbers and blackwood issues. The meeting was in response to my recent commentary about public subsidies and pricing policies. It was an informal meeting with no minutes recorded. Here is a brief summary of what I learnt and concluded:

Business model

(NB. The special timbers industry appears to have convinced many people that paying real market prices for special timbers sawlogs would destroy the industry! While opening up the special timbers market is vital for the success of private special timbers growers.)

Supply

(NB. Most of these plantations were located at Beulah, south of Sheffield on a site unsuited to growing commercial blackwood, using a complex and risky silvicultural model).

The future

This cavalier attitude to Tasmanian farmers and the special timbers industry ignores the fact that New Zealand farmers have been successfully growing blackwood for the past 30 years. Also as I have noted previously, when New Zealand blackwood expert Ian Nicholas last visited Tasmania in 2011 he was very frustrated and disappointed with the way the blackwood industry was being managed. He thought farm-grown blackwood had a great future in Tasmania. In fact it was Ian’s enthusiasm that got me thinking about a growers cooperative. And finally I am not aware of anyone in Tasmania (including FT) applying the successful New Zealand model for growing blackwood including the use of the Three Principles, so significant opportunity remains for further technical development and understanding.

The proposition that FT must manage its special timbers business activities as a non-profit community service is extraordinary and certainly deserving of the commentary and criticism in The Mercury Editorial of September 24, 2011 “Strong medicine for GBEs”.

The proposition that the special timbers industry cannot survive paying real market sawlog prices is logically self-contradictory and straight economic nonsense. Only real market prices can determine the viability and sustainability of the special timbers industry.

The proposition that Tasmanian farmers should be denied the opportunity of growing commercial blackwood in contrast to their New Zealand peers is an extraordinary expression of State forest policy.

If we were talking about any other primary industry such as beef, dairy, vegetables or fruit Tasmanian farmers would be marching on Parliament house. Fortunately, for example, we do not have a non-profit dairy GBE, but many farmers have an intimate knowledge of dairy markets and a long history of running profitable dairy farms. Unfortunately we do have a non-profit forestry GBE, whilst few farmers have much knowledge of forestry markets and little history or understanding of how to profitably grow trees for wood production.

This must now change because profitable, commercially-focused private growers now supply the vast majority of wood grown and harvested in Australia. Why do we therefore persist with State forest agencies that are managed on any other basis, while denying our farmers commercial opportunities, and wasting taxpayers money?

The special timbers and blackwood industries remain in serious crisis with things about to get a whole lot worse, with no indication of any positive change.

As we were leaving the meeting one of the FT representatives asked me whether I thought the TFA would succeed and save the forest industry. I thought it was a curious question given that I had just experienced a perfect 30 minute demonstration of exactly why the forest industry is in its current crisis, and why the TFA faces significant challenges.

Leave a comment

Posted in Commentary, Forestry Tasmania, Markets