Here’s a summary of tender results for blackwood logs sold by Island Specialty Timbers (IST) for the 2013-14 financial year. In the absence of any IST Market Report or any better market information, this small dataset is as good as it gets.

Island Specialty Timbers, an enterprise of Forestry Tasmania, was established at Geeveston in 1992 to increase the recovery, availability and value of specialty timbers from harvesting activities in State forests.

Unfortunately this laudable “mission statement” is not translated into anything concrete or measureable like a business plan. Are these objectives being achieved? What are the measurable performance criteria? How has performance changed over the years? Unfortunately IST does not produce any annual reports, market reports or sales summaries. Also Forestry Tasmania does not report separate financial results for its special timbers activities including IST. So while the “mission statement” is couched in pseudo-commercial language, unfortunately IST exhibits all the hallmarks of a politically motivated public relations exercise.

How do special timbers contribute to Forestry Tasmania’s profitability?

Such a non-commercial, anti-competitive environment makes it difficult to convince farmers that the forest industry is about business and not politics.

It is also curious that although over 80% of the volume of special timbers sold by Forestry Tasmania is blackwood, blackwood makes up only a minor component of the volume of logs tendered by IST every year.

Note that all of the logs and wood sold by IST comes from the harvesting of public native forest. Remember also these tender prices are effectively mill door prices that already include harvesting and transport costs. They are not stumpage prices.

Still I am grateful for the small scraps of commercially useful information that IST provides. This is my attempt to summarise these scraps for the past 12 months.

Summary

For the year 2013-14 a total of 12 blackwood logs were put up for tender by IST. Three of these logs, including the single log in the June 2014 tender, failed to sell. The total value of blackwood logs sold at tender for 2013-14 by IST was $20,800.

The highlight for the year were two very large tear-drop grain logs from the one tree which sold for $9,600 and $7,500 ($2,900 and $2,750 per cubic metre respectively) or a total of $17,100 for 6.04 cubic metres of log from the one exceptional tree. The combination of feature grain, good log quality and large size clearly attracts a significant price premium.

With such incredible prices the obvious question is can blackwood of this size and quality be grown on private land? There are a few key issues that need to be discussed:

Size

The butt log from the above tree had a diametre of over 1 metre, with a total combined merchantable length of 9 metres. Even at the top of the top log the diameter was 83 cm! That is a big blackwood by anyone’s reckoning. Such a log could really only be grown in a (public or private) native forest environment. So yes! Private native forest could be managed to grow blackwood of this size and value given enough time and good management. The goal in blackwood plantations is to produce trees with a diameter at breast height (dbh) of 60 cm in about 35 years. It would take at least 50-60 years to grow a 1 metre diameter blackwood even in a fast-growing environment.

Figured grain

The other key factor with the above logs was the tear-drop grain. Figured grain of any sort is relatively rare in blackwood, tear-drop grain being more rare than fiddleback. Little research has been done on figured grain in trees anywhere in the world. My own belief is that it is both genetic and physiological in origin. Just about all trees have some fiddleback in their stumps as a response to physiological stress. If figure has a genetic component to its origin then there is the potential for cloning. I know a few people in Tasmania who have spent time trying to clone blackwood fiddleback. If feature grain can be cloned then the prospects for commercial blackwood growers improve dramatically. But cloning will only happen within the context of a private blackwood growers industry.

Plain-grain logs

Seven (7) plain grain blackwood logs totalling 10.0 cubic metres sold at tender during the year for a mean of $390 per cubic metre, or a volume-weighted mean of $370 (see Table 1). Some of these logs may be considered equivalent to those grown in commercial blackwood plantations. Logs ranged in size from 0.57 to 3.46 cubic metres, with the smallest log attracting the biggest unit price of $600 per cubic metre!

TABLE 1

| |

Number |

Average of SED (cm) |

Average of Len (m) |

Average of Vol (m3) |

Sum of Vol (m3) |

Average Unit Price ($/m3) |

Sum of Value ($) |

| Sold |

7 |

59 |

4.1 |

1.4 |

10.05 |

$390 |

$3,707 |

| Unsold |

3 |

59 |

4.5 |

1.5 |

4.35 |

| Plain Total |

10 |

59 |

4.3 |

1.4 |

14.40 |

$390 |

$3,707 |

| Sold |

2 |

88 |

4.5 |

3.0 |

6.04 |

$2,825 |

$17,107 |

| Tear drop Total |

2 |

88 |

4.5 |

3.0 |

6.04 |

$2,825 |

$17,107 |

Notes: SED is log small end diameter, Len is log length, Vol is average log volume.

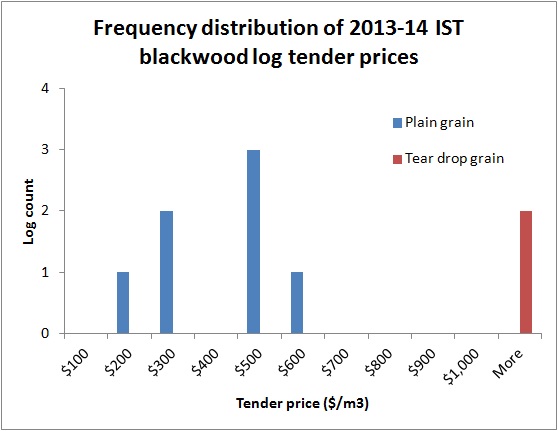

Figure 1 shows the frequency distribution of prices for the blackwood logs sold. For plain grain blackwood logs prices ranged from $180 to $600 per cubic metre. With a mean sale price of $390 per cubic metre, blackwood is attracting a similar price to good quality pruned Macrocarpa cypress sawlogs in New Zealand (see Allan Laurie’s great website). This is surprising given the long heritage of blackwood in the market compared to Macrocarpa which is a relative newcomer to the premium timber market. I have yet to see any equivalent mill-door prices for New Zealand grown blackwood.

FIGURE 1

The dataset was too small to allow any analysis or correlations to be made between price and log quality for the plain grain logs. The fact that the very large 3.5 cubic metre log from the April tender, by far the biggest plain grain log for the year, sold for only $430 per cubic metre indicates that log size by itself does not necessarily attract a price premium.

It seems unlikely that this tiny set of market-based blackwood log prices is representative of the broader blackwood market, given that they represent just 0.18% of the annual blackwood harvest (excluding the unknown volume sold from private property). I suspect the IST tenders attract only a very limited range of small, custom buyers with limited purchasing power.

It would certainly improve market transparency and stimulate greater investor confidence if IST would tender more blackwood and demonstrate real commercial focus. Increasing the blackwood volume tendered to even 100 cubic metres per year would be a good start. At a bare minimum IST could produce an annual summary of tender results.

In the mean time I look forward to providing another summary of IST blackwood tender results next year.

At $390 per cubic metre a mature blackwood plantation is still valued at over $100,000 per hectare!

Now how do I get Tasmanian farmers interested?

Blackwood sawmillers

Private Forests Tasmania (PFT) has just released an updated Tasmanian Primary Wood Processor Directory.

http://www.pft.tas.gov.au/index.php/publications/market-information

The directory is a listing of 45 of the estimated 57 primary wood processing businesses believed to be operating within the State of Tasmania at the time of publication.

The directory has been primarily developed to help private forest owners with logs for sale to identify potential buyers. As well as enabling the forest owner to more easily locate and contact primary wood processors, it also identifies the log types purchased by them.

The directory also helps the listed primary wood processors to source logs from the Tasmanian private forest estate.

It isn’t at all clear to me how the directory helps the listed primary wood processors to source logs from the Tasmanian private forest estate, but anyway….

18 of the 45 listed processors indicate that they want to buy blackwood logs from private landowners. To find these processors simply download and open the document in Adobe Reader. Once the document is open press the Ctrl+Shift+F keys together on your computer. In the search box type “blackwood” and hit the Search button. All 18 instances of the word “blackwood” will now be shown.

ERRATUM: My apologies! I have just realised that three of the primary processors in the Directory list “special species” without listing blackwood separately. I assume these three processors include blackwood in their definition of special species. So that makes a total of 21 of the 45 listed processors are looking to buy blackwood logs from private growers/farmers. That is a very crowded market!!

That there are so many sawmillers around Tasmania looking to buy blackwood logs from private landowners I find very encouraging.

Clearly there is good demand for blackwood timber.

But what size and quality logs, and at what price? What markets are these processors accessing? These are critical questions that need answers.

If blackwood is Australia’s premier appearance-grade timber species then how do we build this industry into something proud and profitable?

How do we get greater transparency and tradability into the blackwood market?

How do we put the blackwood market on steroids?

I don’t mean artificially inflate the demand. I mean create much greater transparency and tradability into the blackwood market so landowners start to see some realtime market activity. Only then will landowners begin to think about investing in the future of blackwood.

How do we get farmers to make a 30-40 year investment commitment to grow more blackwood for the future as both remnant blackwood forest and in plantations?

ANSWER: By giving farmers as much incentive and positive market sentiment and feedback as we possibly can. Once farmers begin to see the blackwood market operating like other rural commodity markets then we might have some hope.

Every day we see blackwood timber making its way to the very highest of the wood value-adding markets both in Australia and increasingly overseas. Markets such as premium furniture, veneers, and musical instruments. So why isn’t this market demand stimulating grower interest? Why doesn’t Tasmania have a thriving blackwood grower community? Is growing blackwood a profitable investment for a landowner?

These 18 sawmillers can help answer these fundamental questions.

How many of these 18 processors are thinking about the future of the blackwood industry as anything other than a clean-up salvage operation?

Are they waiting for the Government to solve the problems of the forest industry, or are they prepared to take responsibility themselves and take some action?

These blackwood sawmillers are fundamental to the future success of Tasmania’s blackwood industry. But things need to change and change radically.

At the moment the blackwood market is completely obscure, which inhibits growth and investment in the industry.

The day that I can write my first Blackwood Market Report for Tasmanian Country will be a significant day for the blackwood industry.

There is plenty of potential and many opportunities with blackwood provided Tasmanians are prepared to help see them happen.

What’s in it for these sawmillers?

Or are we going to surrender our blackwood heritage to the New Zealand farmers?

I would like to hear some thoughts and ideas from these blackwood sawmillers. Reply to this blog, or phone or email me so we can have a discussion.

Cheers!

Leave a comment

Posted in Commentary, Markets, Prices

Tagged Private Forests Tasmania